The clean energy transition depends entirely on a handful of minerals extracted from a small number of countries under conditions most procurement teams have never had to model. That is a supply chain problem that is now an energy strategy problem.

Industrial Energy · Business Infomatics Research Desk

Copper, lithium, cobalt, nickel, and rare earth elements are not abstractions in an energy policy document. They are the material inputs that determine whether a solar panel gets built, whether an EV battery performs to specification, whether a wind turbine can be commissioned on schedule. For the last decade, the dominant conversation in industrial energy has been about generation economics — the cost of solar, the levelised cost of wind, the financing structures for offshore development. That conversation is not wrong, but it has been incomplete.

The conversation that energy executives and the procurement officers who support them now need to be having is about where the physical inputs to the energy transition come from, who controls those supply chains, and what the realistic risk of disruption looks like over a ten-year planning horizon. The answers are uncomfortable.

The Concentration Problem, Quantified

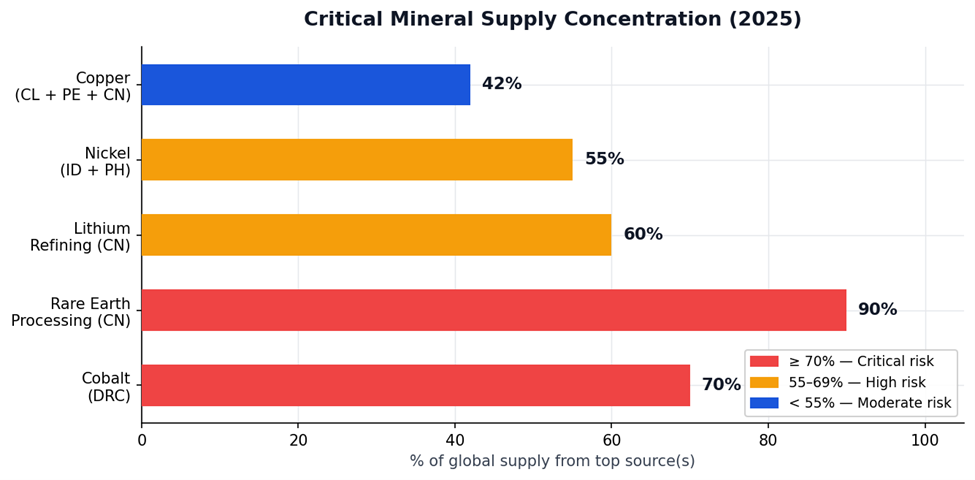

The IEA's 2025 Critical Minerals Outlook documents the scale of the challenge with unusual precision. The Democratic Republic of Congo produces approximately 70 percent of the world's cobalt. China refines roughly 60 percent of the world's lithium — including a majority of the lithium extracted in Australia and Chile — before it enters the global battery supply chain. China also accounts for nearly 90 percent of global rare earth element processing. Indonesia and the Philippines together produce the majority of the world's nickel.

Source: IEA Critical Minerals Outlook 2025. Red = critical risk (≥70% concentrated in single source).

70% of global cobalt supply originates from a single country. (IEA, 2025)

These are not margins that permit comfortable diversification over the timelines most energy transition plans assume. A procurement team managing aluminium supply can typically identify alternative suppliers within the same continent with comparable lead times. Rare earth element processing has no equivalent alternative supply chain at scale anywhere outside China at present, and building one takes a decade of capital investment and regulatory permitting that has not yet started in most jurisdictions.

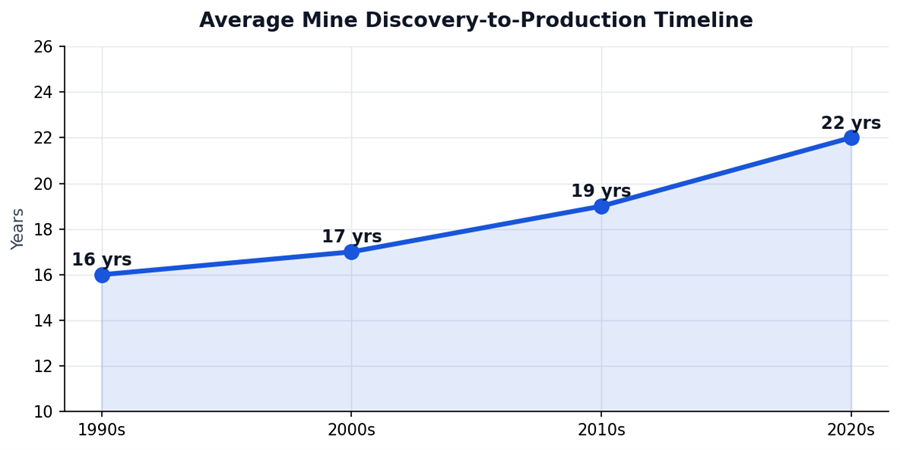

The copper picture is different in character but equally concerning in magnitude. The average time from discovery to first production for a major copper mine has increased from sixteen years in the 1990s to over twenty years today — while demand projections suggest copper demand could double by 2035.

Average discovery-to-production timeline has lengthened by 6 years since the 1990s — compounding the supply gap.

The Supply Gap That's Already Opening

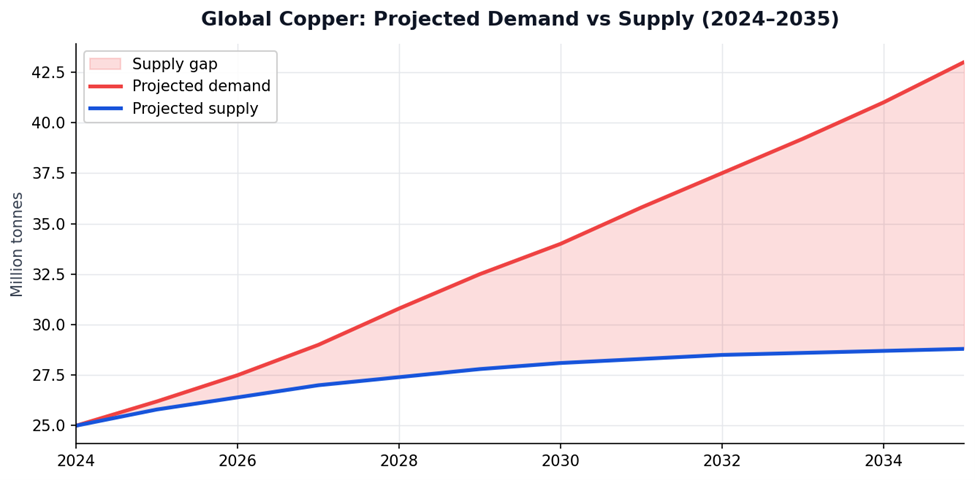

Demand projections from the Energy Transitions Commission suggest copper demand could double by 2035. Supply cannot grow that fast under current conditions — and the resulting gap will become a primary constraint on the pace of the energy transition itself.

Projected copper demand vs. supply trajectory 2024–2035. The widening gap represents unmet energy transition capacity. Sources: Energy Transitions Commission, Wood Mackenzie.

How This Shows Up in Project Execution

The disruption that concentrated supply chains create does not always arrive as a dramatic shortage. More often it arrives as cost escalation, lead time extension, and specification compromise that accumulates across a project until the economics look materially different from the feasibility study.

Battery-grade lithium prices rose approximately 500 percent between 2020 and 2022 before retreating — a swing large enough to render several utility-scale storage projects financially unviable at the pricing assumptions used when they were approved. The projects that survived that cycle were the ones whose developers had locked in either supply agreements or price indexing mechanisms before the market moved.

$360B+ committed globally to critical mineral supply chain development by G7 governments through 2030. (IEA, 2025)

What Serious Supply Chain Management Looks Like

Visibility Before Mitigation

You cannot manage a supply chain risk you cannot see. A surprising number of energy companies do not have granular mapping of the critical mineral content in their equipment and construction contracts beyond the tier-one supplier level. The battery is visible. The cathode material supplier is visible. The refinery that processed the lithium carbonate is often not. Building that visibility is the prerequisite for everything else.

Long-Horizon Contracting Is Being Repriced

The traditional procurement model in industrial energy valued competitive tension at each procurement cycle over supply security. That balance is shifting. Several large renewable developers have now made multi-year offtake agreements directly with mining companies a standard element of their project financing structure, rather than an optional risk mitigation measure.

Recycling Is Not a Near-Term Fix — But Needs Investment Now

Battery recycling operations in the UK and Germany are processing meaningful volumes, and the material recovered is re-entering supply chains. But volumes are small relative to primary demand. Energy companies investing in battery storage today are making decisions whose recycling implications will not materialise for ten to fifteen years. The organisations building recycling capability into their asset management plans now will be better positioned when those assets reach end of life.

The Geopolitical Layer

The export restrictions China applied to gallium and germanium in 2023 — and the critical mineral restrictions that followed in 2024 — were demonstrations of policy. This does not mean supply chains will be severed. But it does mean that supply chain risk analysis cannot be done purely on a commercial basis without a view on the political conditions that determine whether commercial arrangements remain enforceable.

The energy transition is happening. The economics of renewable generation are settled. What the critical minerals picture changes is the risk profile of energy transition investments — in ways that are not yet reflected in the planning assumptions of most organisations. The organisations managing this well have decided that supply chain strategy is a strategic function, not an operational one.